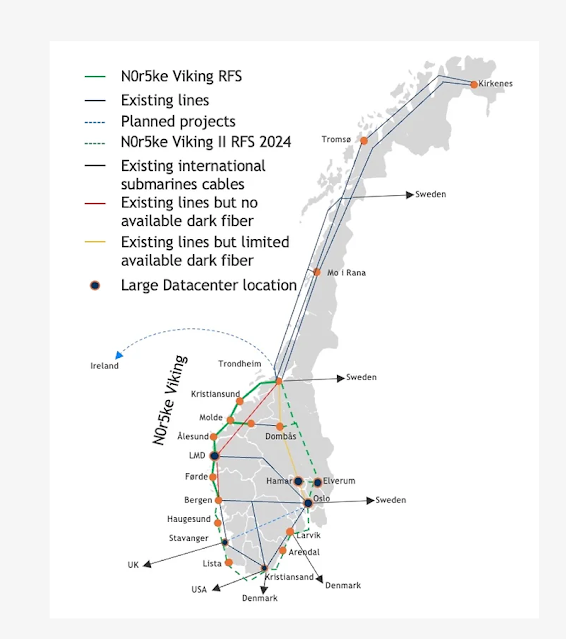

Eastern Light is building a hybrid subsea-terrestrial dark fibre ring connecting Sweden, Finland, the Baltics, Germany, Denmark, and Norway. This morning I interviewed their sales director to better understand this ambitious project. The fibre pair count is 3x 144 pairs or 432 in total. No lit optical circuits or wavelengths will be sold. Instead, customers will be leasing or purchasing via IRU fibre pairs that they will light using their own equipment. There are ILAs for the subsea spans located on islands, but the short distances make them an option, not a necessity. However, some customers will undoubtedly prefer buying less and optically amplifying to juice the transmission rates. Because it is a dark fibre network, the customer base will be predominantly hyperscalers, big carriers including the incumbents (Telia's international network is old), university research consortiums, governments including their national militaries, NATO, and banks. In particular, hyperscalers are e...

.jpg)