Subsea Cable News - AAE1 Down & Pearls 2Africa Ready 2025:4

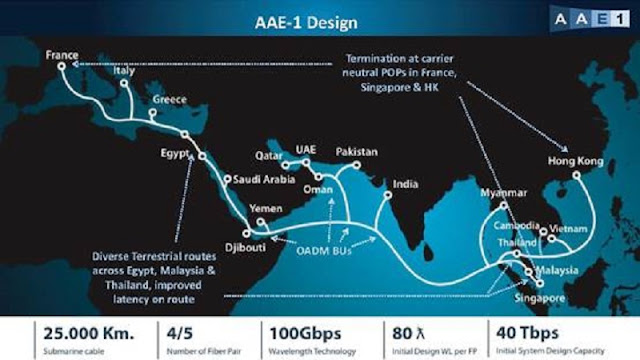

Bad news and also mildly bad news. AAE1 is down due to a fault in the Red Sea located between the Zafrana, Egypt and Saudi branching units. The outage began December 31st. Pearls 2Africa (depicted in the map) will go live near year's end, but it has only one fibre pair down the African East Coast from Oman to Kenya. China Mobile owns it. The Big Picture is that the subsea cable world is facing a tough year. Right now Peace is the only high capacity cable live connecting Marseille to Singapore via the Red Sea. AAE1 is down. 2Africa, SWM6, Blue-Raman, and probably IEX cannot be completed due to the threat of Red Sea missile strikes. We can only hope that diplomacy results in safe passage for the cable ships. Otherwise persistent capacity shortages will only grow worse. I do expect AAE1 to be repaired within eight weeks as a cable ship can bypass Yemen via the Suez cable. But beware most cable ships are deploying new cables like Blue and Medusa. My guess is that the Indian owned cabl...